BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from April 1, 2018 - April 7, 2018

Separate the Wheat from the Chaff: More Brainstorming on Implementing Robotic Finance

Here is more information related to implementing robotic finance and an updated version of my document Guide to Implementing Robotic Finance.

I think that Inline XBRL will help enable a transition from current accounting and financial report creation processes and robotic finance. In addition, there is a boatload to be learned form the Inline XBRL financial reports of public companies that have been submitted to the SEC. While it can be a challenge today to "separate the wheat from the chaff", here is why I think what I think.

First, you have to "look around" the quality issues, the information representation issues, the issues with the US GAAP XBRL Taxonomy, and other factors related to the XBRL-based financial reports that public companies submit to the SEC. Don't let those things distract you.

If you look at the reports of public companies that don't have errors and if you look at disclosures that do not have errors there is a lot that can be learned. There are many, many reasons why the XBRL-based reports of public companies have issues. But there are just as many of good examples that provide excellent learning opportunities.

Second, you have to "look around" the software issues of the software vendors and filing agents that have created software to support the creation of XBRL-based financial reports. Most have not taken a long-term view of the opportunity. Most have built "bolt on" solutions that add to existing processes that make XBRL seem like more work rather than expose the true opportunity. Don't let that distract you.

Third, you have to "look around" the fact that XBRL-based reports of public companies are not leveraging metadata appropriatly and the general lack of metadata.

If you don't understand what I am talking about, I would encourage you to read the document Closing the Skills Gap. That will help you get better dialed into what is really going on.

Now, I did some experimenting with Inline XBRL (see points 1 through 6). I am continuing that experimentation here on public company financial reports submitted to the SEC. The prior examples where testing smaller test documents that I had created to examine specific things. So here I am looking at the same idea of contrasting raw XBRL to Inline XBRL; but I am doing this experiment with a 10-K filed with the SEC by a public company. Here is the filing I am looking at.

- Raw XBRL: I start here with the raw XBRL. Now, this raw XBRL was not created by the filer, it was auto-generated by the SEC. This company submitted their report in the Inline XBRL format.

- Inline XBRL (in Inline XBRL Viewer): This is the Inline XBRL as viewed using the SEC provided Inline XBRL viewer.

- Inline XBRL (not in viewer): This is the same Inline XBRL document but not viewed using the SEC Inline XBRL viewer; this is the document you would work with to extract information from the Inline XBRL using a computer based process.

- Inline XBRL auto-generated from Raw XBRL: This is Inline XBRL that was auto-generated by XBRL Cloud from the raw XBRL auto-generated by the SEC from the Inline XBRL submitted by the filer. This rendering is pretty readable but does have some readability issues.

- Extraction of Facts: This is a ZIP archive that contains an Excel spreadsheet with macros that extract facts from raw XBRL or inline XBRL. The tool will extract facts from #1, #3, and #4 above. (Note that there appears to be a bug in the XBRL Could auto-generated inline XBRL. The first two documents report 2,182 facts but the third has 1,860 facts returned. I am looking into why this is happening.)

So the point here is that extracting information from Inline XBRL is just as easy as extracting information from Raw XBRL. You should get the exact same results when information is queried in either syntax; which syntax you use does not impact the meaning of the information represented.

A public company financial reoprt filed as part of a 10-K is about as complex document that I can imagine. What might be more complex is the management discussion and analysis document which is also part of an SEC 10-K but does not need to be represented using XBRL currently.

In this prior analysis I was using smaller documents than a 10-K financial report. I did that to make creating all the business rules to verify the facts reported in the document easier. The only difference between the documents used in the prior analysis and the 10-K financial report is the volume of disclosures. The fact is that the smaller test documents that I used are more complex than the 10-K financial report. Why? Because I included some additional information patterns that are not used in the typical 10-K financial report.

Charlie

in Becoming an XBRL Master Craftsman, Digital Financial Reporting

|

Charlie

in Becoming an XBRL Master Craftsman, Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Quarterly XBRL-based Public Company Financial Report Quality Measurement (Mar 2018)

The following is a summary of the quality measurements of XBRL-based financial reports submitted to the SEC as of March 31, 2018. The following Excel spreadsheets and other documents provide details related to these quality measurements:

- Narrative which further explains these measurements

- ZIP file containing Excel spreadsheet with details of errors

- ZIP file containing Excel spreadsheets which has pretty good (i.e. not commercial quality, but close) working validator and validation of 3,945 XBRL-based financial filings, about 67% of all such reports

- 10-K metadata for 6,005 public companies (easy to work with XML infosets; fairly large, takes about 10 minutes to download)

- Extraction tool

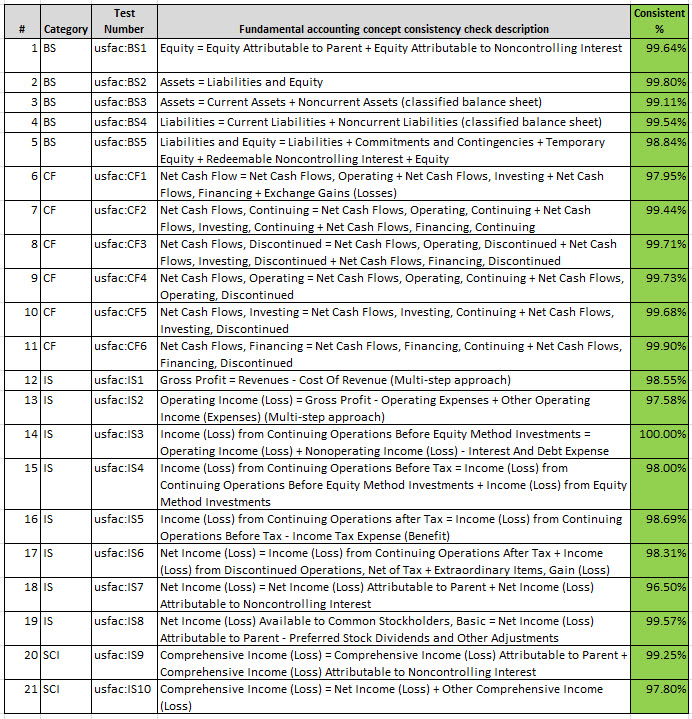

In summary, fundamental accounting concept relations quality has steadily improved each year as can be seen by the three year comparison. On an individual test basis, each of the 22 relations tests is 98% consistent with what is expected. 88.5% of all XBRL-based financial reports are consistent with all 22 relations tests as would be expected. The goal as I see it is that all XBRL-based financial filings are 99.99966% consistent with expectations (six sigma).

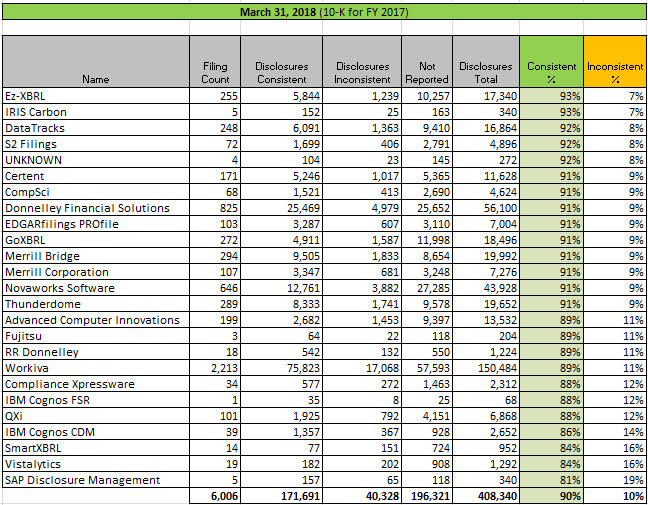

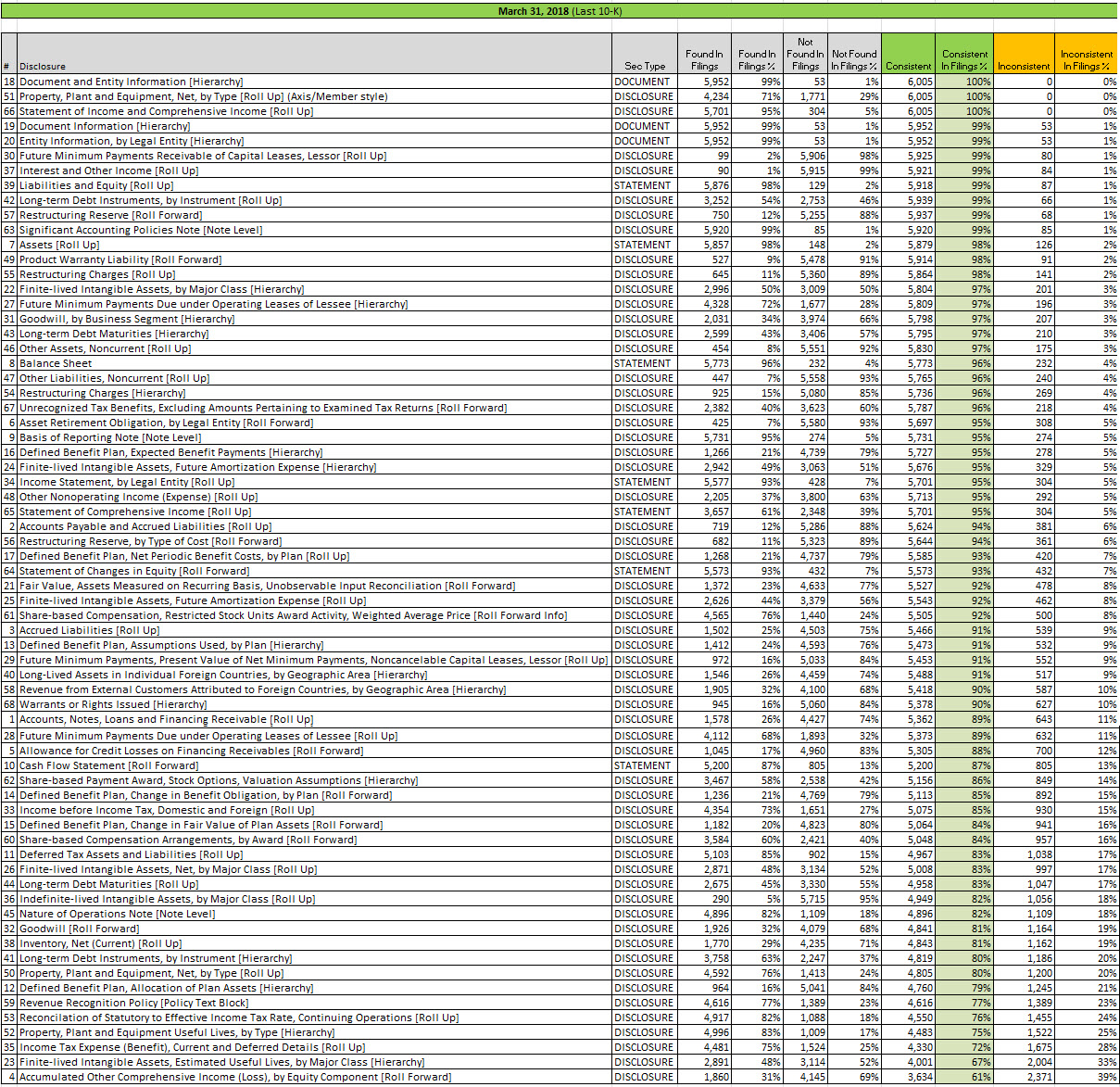

I have added measurements of what I call the disclosure mechanics of 65 disclosures. Disclosure mechanics quality has increased from 88% to 90% for the 65 disclosures I am measuring. Again, the goal is six sigma for every disclosure reported.

The following are graphical summaries:

Fundamental accounting concept relations for last 10-K or 10-Q filed by generator of the report:

(Click for larger image)

(Click for larger image)

Fundamental accounting concept relations by relation test (same filings as above):

(Click image for larger view)

(Click image for larger view)

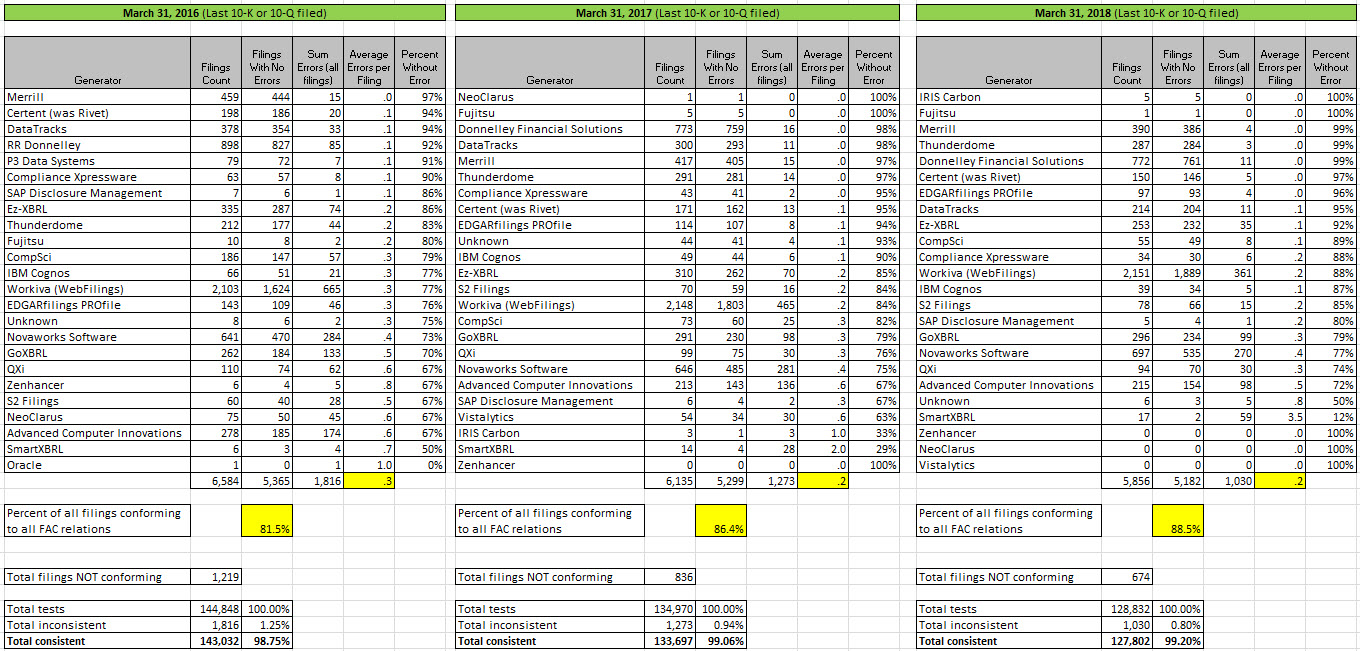

Comparison of 2016, 2017, and 2018 fundamental accounting relations results:

(Click image for larger view)

(Click image for larger view)

Disclosure mechanics by generator results from analysis of last 10-K filed with SEC as of March 31, 2018:

(Click image for larger view)

(Click image for larger view)

Disclosure mechanics results by disclosure:

(Click image for larger view)

(Click image for larger view)

I will likely put together a narrative that explains these measurements in more detail.

**********************PRIOR RESULTS**********************

Previous fundamental accounting concept relations consistency results reported: November 30, 2017; August 31, 2017; May 31, 2017; March 31, 2017; November 28, 2016; August 31, 2016; June 30, 2016; March 31, 2016; February 29, 2016; January 31, 2016; December 31, 3015; November 30, 2015; October 31, 2015; September 30, 2015; August 31, 2015; July 31, 2015; June 30, 2015; May 29, 2015; April 1, 2015; November 29, 2014.

Charlie

in Becoming an XBRL Master Craftsman, Creating Investor Friendly SEC XBRL Filings, Digital Financial Reporting

|

Post a Comment

| Email

| Print