BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from June 24, 2018 - June 30, 2018

Quarterly XBRL-based Public Company Financial Report Quality Measurement (June 2018)

The following is a summary of the quality measurements of XBRL-based US GAAP financial reports submitted to the SEC as of June 30, 2018. The following Excel spreadsheets and other documents provide details related to these quality measurements:

- Positive results from tests (i.e. proof): Set of Excel spreadsheets contained in a ZIP archive that lets you duplicate testing, proving that over

- Negative results from tests (i.e. confirmed errors): Details of 100% of the confirmed errors. 974 errors contained with 639 filings.

- Accounting errors discovered during validation process: This PDF provides details of rather obvious accounting errors that exist in the financial reports of public companies. This validation process leads to the detection of such errors.

- Prototype validation tools: Some working prototype, proof-of-concept validation tools you can use. Only provided for one reporting style. I added a "line of reasoning" text file that helps you review the validation results.

- US GAAP Rules: Current publicly available version of the validation rules by reporting style for US GAAP. As of March 31, 2018. Contact me if you want the most current version.

- IFRS Rules: Current publicly available version of the validation rules by reporting style for IFRS.

- Templates: A financial report can be broken down into fragments. The same techniques for validating the primary financial statements also applies to other disclosures, only the rules are different.

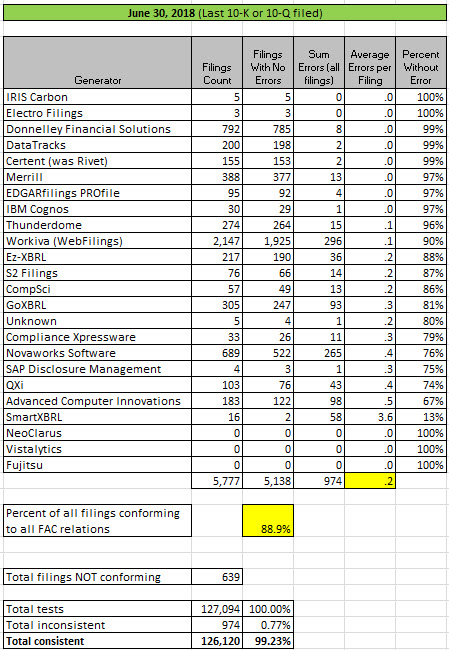

US GAAP fundamental accounting concept relations continuity cross check validation results for last 10-K or 10-Q filed by generator of the report as of June 30, 2018:

(Click image for larger view)

(Click image for larger view)

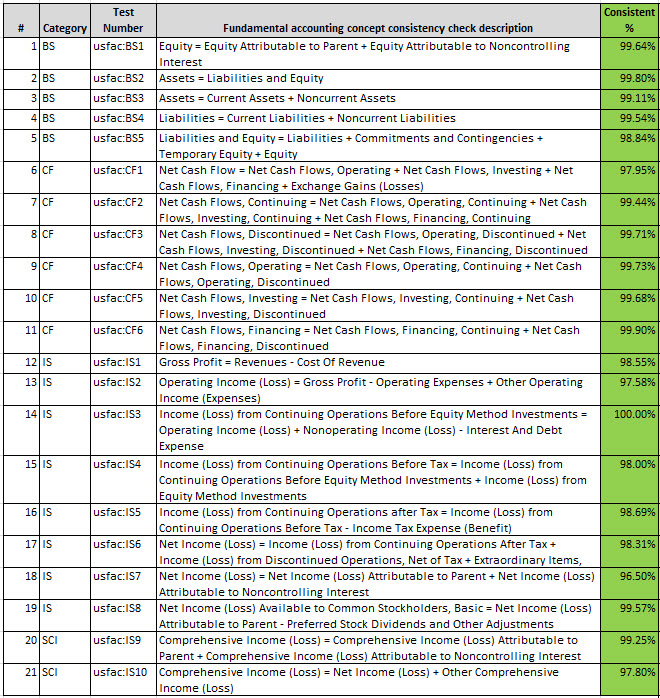

US GAAP fundamental accounting concept relations continuity cross check by logical accounting relation tested (same filings as above):

(Click image for larger view)

(Click image for larger view)

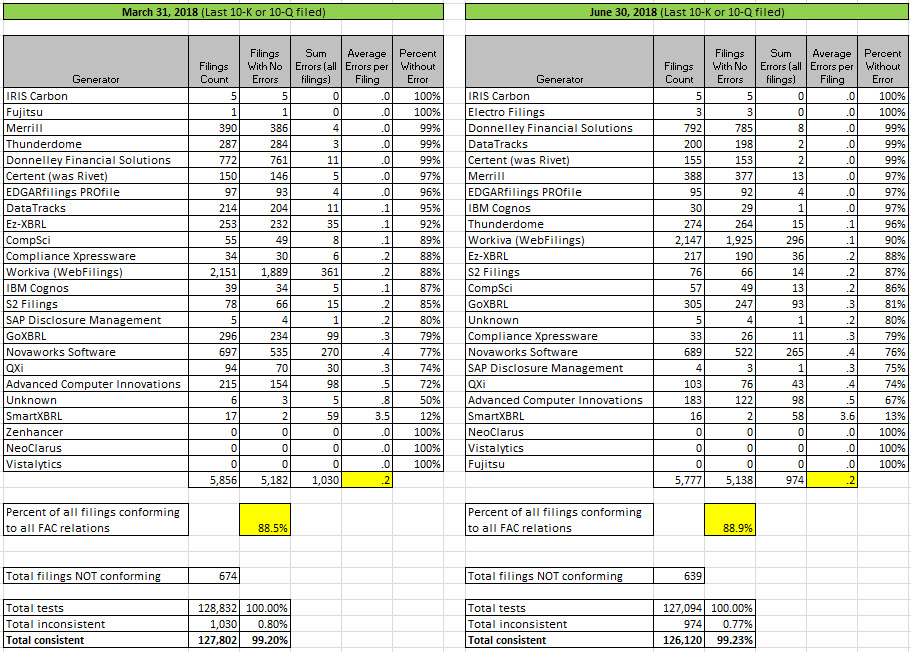

Comparison of the prior results as of March 31, 2018 and the current results as of June 30, 2018 by generator:

(Click image for larger view)

(Click image for larger view)

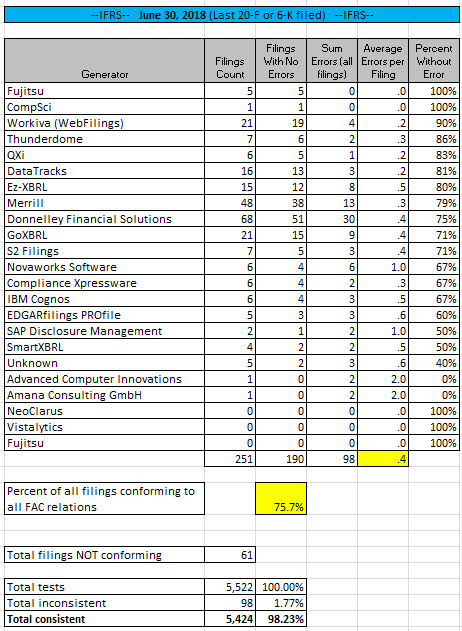

NEW!!! IFRS Fundamental Accounting Concept Relations (Work in Progress) I am going to start testing IFRS filings also! These results are a work in progress but very accurate. I have all the balance sheet and cash flow statement reporting styles working; but I only have a couple of the income statement reporting styles working.

(Click Image for Larger View)

(Click Image for Larger View)

**********************PRIOR RESULTS**********************

Previous fundamental accounting concept relations consistency results reported: March 31, 2018; November 30, 2017; August 31, 2017; May 31, 2017; March 31, 2017; November 28, 2016; August 31, 2016; June 30, 2016; March 31, 2016; February 29, 2016; January 31, 2016; December 31, 3015; November 30, 2015; October 31, 2015; September 30, 2015; August 31, 2015; July 31, 2015; June 30, 2015; May 29, 2015; April 1, 2015; November 29, 2014.

Information helpful to understanding errors, learn how to create quality XBRL-based digital financial reports.

Blueprint for Creating Zero-defect XBRL-based Digital Financial Reports, helps you understand how to test other aspects of a digital financial report.

Computer Empathy, the best way to get dialed into accounting, reporting, auditing, and analysis in a digital environment.

McKinsey: Five lessons from history on AI, automation, and employment

In the article Five lessons from history on AI, automation, and employment, Susan Lund and James Manyika provide a framework to think about the changes that AI will bring to the accounting profession over the coming years.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print